Reducing insulin costs is one of the most pressing concerns for people with diabetes in the United States today. If you or someone you care about relies on insulin to control blood sugar, you already understand how costly it can be — and how alarming it feels when the bill surpasses what you can afford. The good news is that genuine help exists, and recent research confirms that cost-saving policies are working.

A landmark study published in JAMA Internal Medicine in April 2026 tracked nearly 4.8 million Medicare patients with type 2 diabetes from 2019 to 2023. It found that federal policies capping insulin out-of-pocket costs at $35 per month were linked to significant savings, more consistent insulin use among those already prescribed insulin, and measurable improvements in blood sugar control — though the research also identified a modest rise in severe low blood sugar events, highlighting that any changes in insulin access need careful management. Whether you have Medicare, private insurance, or no insurance at all, this guide covers the most effective ways to lower what you pay for insulin.

↓ Jump to: Frequently Asked Questions About Insulin Costs

Quick Reference: Top Ways to Reduce Your Insulin Costs

| Strategy | Who It Helps Most |

|---|---|

| Medicare $35/month insulin cap (Part B & D) | Medicare enrollees |

| State insulin copay caps | Privately insured patients in 29 states + DC |

| Manufacturer assistance programs | Uninsured or underinsured patients |

| Biosimilar insulins (including interchangeable options) | Anyone whose plan covers biosimilars |

| Lower-cost human insulin (e.g., ReliOn NPH or Regular) | Uninsured or high-deductible patients (with doctor guidance) |

| Pharmacy price comparison tools | All patients paying cash |

| 90-day supply fills | Patients on stable, long-term regimens |

| Ask your doctor for samples | Newly starting insulin, tight budget |

Why Is Insulin So Costly in the United States?

Insulin has been used to treat diabetes since 1922, more than 100 years ago. Yet the price Americans pay for it has skyrocketed. Between 2002 and 2013 alone, the cost per milliliter of insulin nearly tripled, rising from about $4.34 to $12.92. That trend continued for years afterward.

Unlike many countries where governments directly negotiate drug prices, the US system has traditionally allowed insulin manufacturers to set their own list prices, and those prices rose sharply over the decades. The result: some patients were paying hundreds of dollars each month just to afford a medication they cannot live without.

A 2019 study in JAMA Internal Medicine found that many patients were rationing insulin — taking less than prescribed — because they could not afford to fill their full prescription. Rationing insulin is dangerous. It can lead to dangerously high blood sugar (above 240 mg/dL or 13.3 mmol/L), diabetic ketoacidosis, emergency room visits, and in severe cases, death. If your blood sugar is running consistently high, inadequate insulin access may be a factor worth discussing with your care team.

The hopeful news: policies at both the federal and state levels have pushed back on these costs, and new research confirms they are making a real difference.

What Is the Medicare $35 Monthly Insulin Cap?

The Medicare $35 monthly insulin cap is a federal policy that limits how much Medicare enrollees pay out of pocket for covered insulin each month — under both Medicare Part B (for insulin used with a pump, covered as durable medical equipment) and Medicare Part D (for insulin dispensed at a pharmacy). It represents one of the most significant changes in prescription drug costs for older Americans in decades.

How the Cap Was Created

The cap was implemented in two phases:

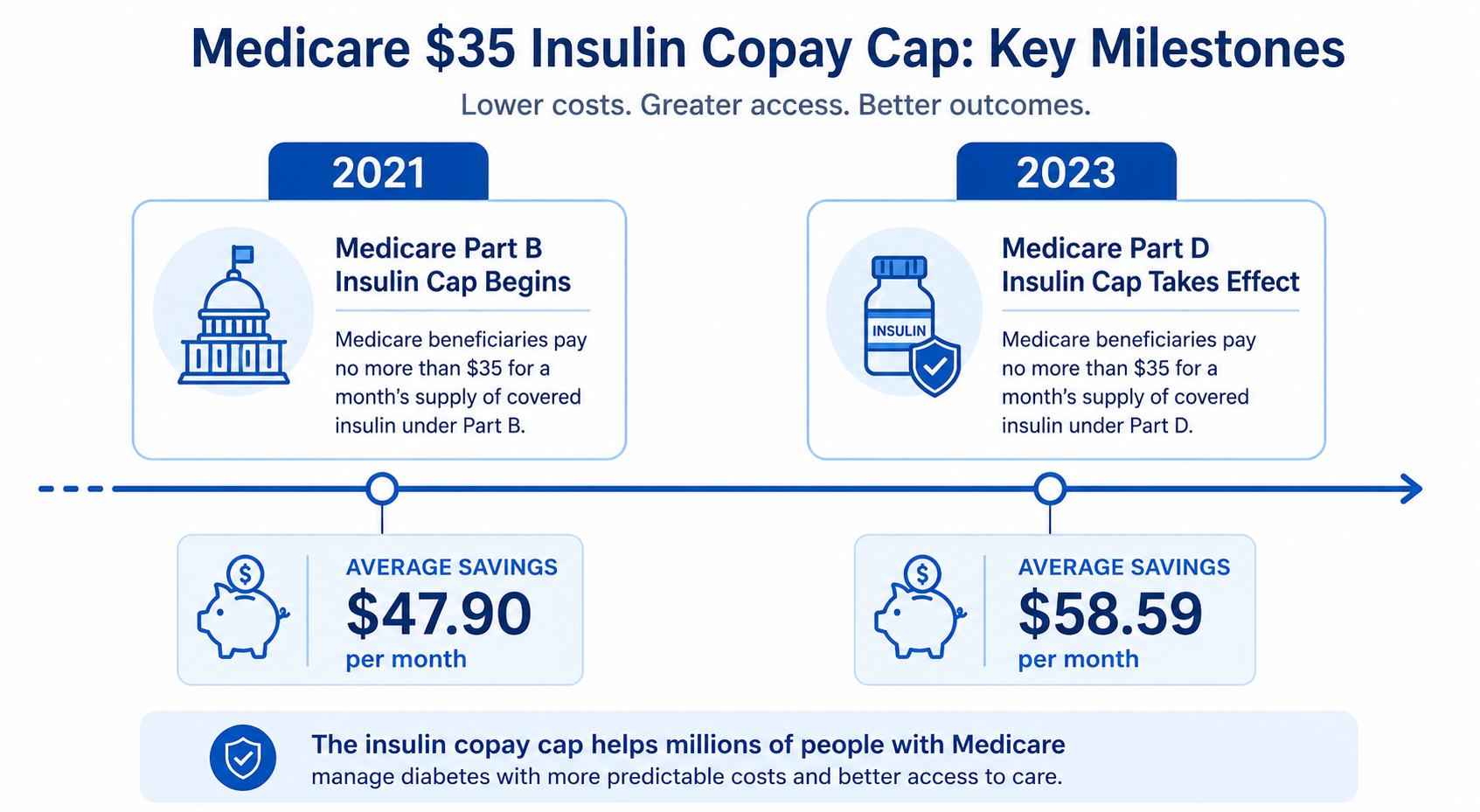

- January 2021: The Centers for Medicare & Medicaid Services (CMS) launched the Part D Senior Savings Model, a voluntary program allowing participating Medicare drug plans to cap insulin copays at $35 per month. By 2022, over 17 million Medicare beneficiaries were enrolled in plans with this protection.

- January 2023: Congress made the cap permanent and universal for all Medicare Part D beneficiaries as part of the Inflation Reduction Act (IRA). No matter which Part D plan you have, your copay for covered insulin is now capped at $35 per month.

What the Research Actually Revealed

The April 2026 JAMA Internal Medicine study by Hong et al. is the most comprehensive independent assessment of these policies to date. Analyzing 4.8 million Medicare patients with type 2 diabetes from 2019 to 2023, it identified four main effects — and one important caution.

First, out-of-pocket insulin spending dropped sharply. Among insulin users, the average quarterly out-of-pocket cost was $192.66 at the start. It decreased by $47.90 after the 2021 cap and by another $58.59 following the 2023 expansion — bringing the cost to about $95.42 per quarter by the end of 2023. Before the cap, 62% of Medicare insulin users paid more than $35 for a 30-day supply; by the end of 2023, fewer than 1% did.

Second, existing insulin users used more insulin. Among patients already filling insulin prescriptions, the average daily dose was 57.38 units before the cap. After 2021, this increased by approximately 1.36 units per day, and by an additional 1.16 units per day after the 2023 expansion. This indicates the cap helped people already on insulin take their full prescribed dose rather than ration it.

Third, blood sugar control improved. In a subset of over 207,000 patients with linked medical records, average A1c — a measure of blood sugar over roughly three months — decreased by 0.06% after 2023, and the percentage of patients with poor blood sugar control (A1c above 9%) dropped by 0.82 percentage points.

Fourth — and worth noting — severe low blood sugar events increased slightly. The quarterly rate of hospitalizations or emergency visits for severe low blood sugar (hypoglycemia) rose modestly after both the 2021 and 2023 cap implementations. This may reflect an important safety trade-off: when patients resume taking their full prescribed insulin dose after a period of rationing, glucose control may improve, but hypoglycemia risk can rise unless doses are reviewed carefully with a healthcare provider.

What the Editorial Adds: Looking Beyond Price

A companion editorial in the same issue of JAMA Internal Medicine by Hung, Inouye, and Durant emphasizes that insulin copay caps should be assessed on more than just their impact on costs. The editorial points out a key limitation: although the $35 cap helped current insulin users stick to their medication more consistently, it did not appear to increase the number of patients starting insulin for the first time.

People with type 2 diabetes who were not yet on insulin did not begin it at higher rates during the study period. This is significant because affordability alone may not be enough to overcome clinical inertia, patient hesitancy, or the need for closer monitoring when starting insulin therapy. The editorial notes that copay caps need to be paired with broader support for patients and prescribers to promote appropriate insulin initiation — not just improved adherence among those already using it. A growing role for GLP-1 receptor agonists and SGLT-2 inhibitors as first-line agents may also be a factor in lower rates of new insulin starts.

What Does the Cap Cover, and Are There Limits?

The $35 monthly cap applies to covered insulin under both Medicare Part B and Part D. Most major insulins, including long-acting and rapid-acting types, are covered under Part D if they appear on your plan’s formulary (drug list). Insulin used in a pump is typically covered under Part B as durable medical equipment.

A few practical clarifications:

- For a standard 30-day supply, you pay no more than $35 for each covered insulin product. A 3-month supply is generally capped at no more than $105 per covered insulin.

- If you use more than one type of insulin — such as both a long-acting and a rapid-acting type — the $35 cap applies separately to each covered product.

- Starting in 2026, some Medicare insulin users may pay less than $35 for selected insulin products if the negotiated price produces a lower cost-sharing amount. For NovoLog and Fiasp, check your plan’s current formulary and pharmacy pricing, because the exact amount may vary by plan and supply format.

- The cap does not cover other diabetes medications, such as GLP-1 drugs or SGLT-2 inhibitors. As the 2026 JAMA study found, spending on these non-insulin drugs increased during the same period that insulin costs decreased, meaning overall medication bills remained high for many patients.

There is additional good news for Medicare patients with very high total drug costs. The Medicare Part D annual out-of-pocket spending cap, $2,000 in 2025, increased to $2,100 for 2026. This limit applies to covered Part D drugs only; it does not include Part B drugs or medications obtained outside the Part D benefit. If your total covered prescription drug costs are high, this annual cap may provide meaningful relief alongside the insulin-specific one.

How Can You Save Money on Your Insulin? Practical Tips for Patients

Even if you are not enrolled in Medicare, there are many proven ways to cut your insulin costs. Here are the most effective strategies.

1. Ask About Biosimilar Insulins — Including Interchangeable Options

Biosimilar insulins are FDA-approved versions of brand-name insulins that are just as safe and effective, often at a lower cost. Think of them as the closest thing to a generic insulin, though the manufacturing process is more complex. Four insulin biosimilars are now FDA-approved in the US:

- Semglee (insulin glargine-yfgn): A biosimilar to Lantus (long-acting), with interchangeable status. Available since 2021.

- Rezvoglar (insulin glargine-aglr): A biosimilar to Lantus (long-acting). Available since 2021.

- Merilog (insulin aspart-szjj): Approved February 14, 2025 — the first rapid-acting biosimilar to NovoLog. Developed by Sanofi and available since July 2025 at $35 or less per month.

- Kirsty (insulin aspart-xjhz): Approved July 15, 2025 — the first interchangeable rapid-acting biosimilar to NovoLog, developed by Biocon Biologics.

Interchangeable biosimilars can generally be substituted at the pharmacy without a new prescription, though this is subject to your state’s pharmacy laws and your insurance plan’s policies. Ask your pharmacist whether substitution is allowed for your prescription and state. Not all plans cover the same biosimilars, so confirm coverage before making the switch.

2. Ask About Lower-Cost Human Insulin Options

Walmart sells older human insulins — ReliOn NPH and Regular — over the counter for about $25 per vial, without a prescription. These are not generic versions of modern analog insulins; they are an older class of human insulin that functions differently. Their timing of action differs from modern analogs, so your dosing schedule and meal timing would need to change. They are not suitable for everyone, and switching without medical guidance can lead to dangerous blood sugar fluctuations. If cost is a serious concern, discuss this option with your doctor before making any changes.

3. Use Manufacturer Patient Assistance Programs

All three leading insulin manufacturers provide programs for patients who cannot afford their insulin:

- Eli Lilly: The Lilly Insulin Value Program limits insulin costs to $35/month for eligible uninsured or commercially insured patients. In 2023, Lilly also voluntarily reduced the list price of its most commonly used insulins by 70%.

- Novo Nordisk: The Patient Assistance Program provides free insulin to eligible low-income patients. Additionally, in 2023, Novo Nordisk capped insulin out-of-pocket costs at $35/month for many patients.

- Sanofi: The Insulins Valyou Savings Program provides discounts on Sanofi insulins for eligible patients. Sanofi also manufactures Merilog, the rapid-acting biosimilar, at $35 or less per month.

You can also visit NeedyMeds.org or RxAssist.org for a comprehensive list of available assistance programs.

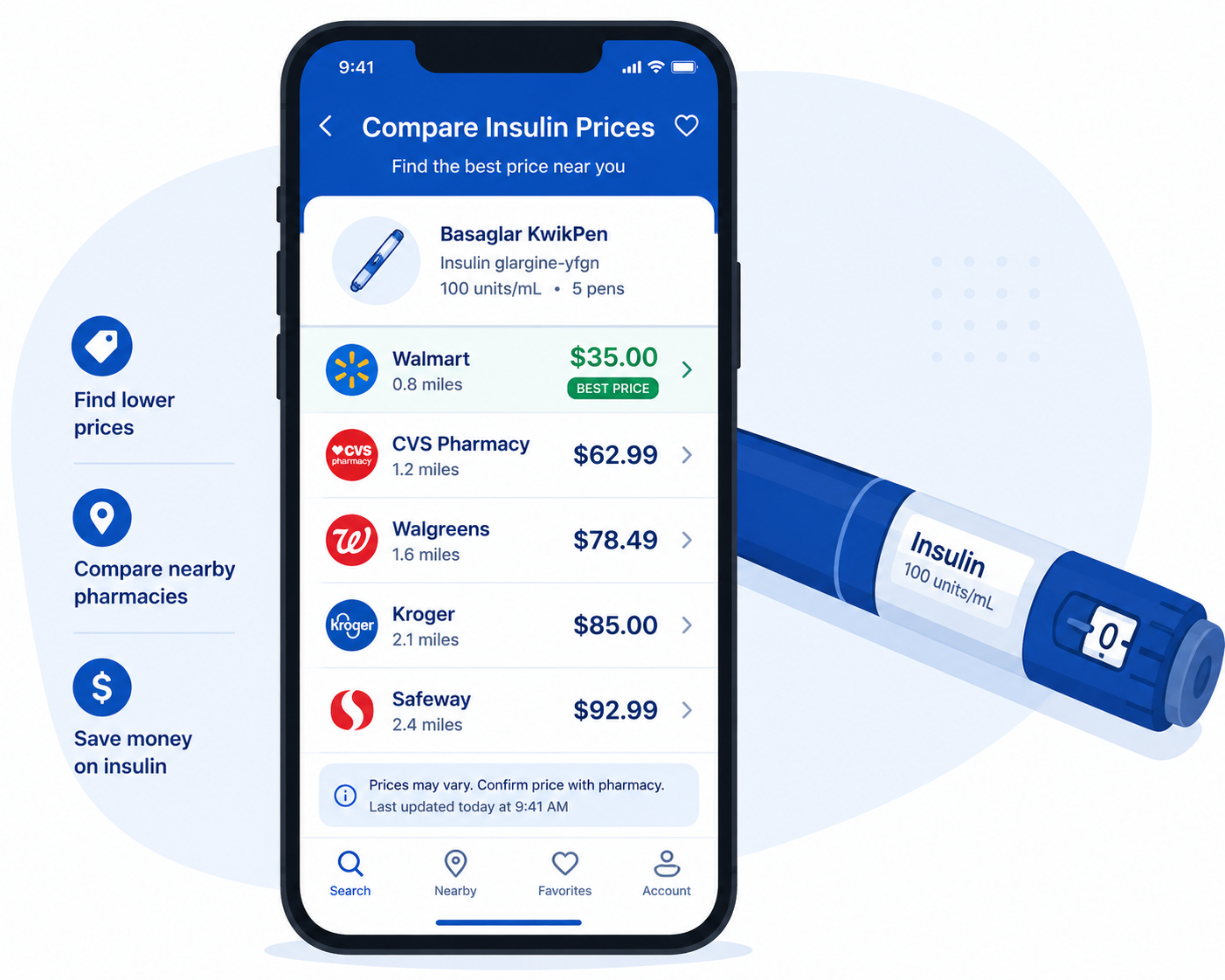

4. Compare Prices at Different Pharmacies

The price of the same insulin can vary dramatically from one pharmacy to another. Free tools like GoodRx, RxSaver, and Cost Plus Drugs let you compare prices in your area before filling your prescription. An independent pharmacy, a warehouse club pharmacy (such as Costco or Sam’s Club), or a mail-order pharmacy may charge significantly less than a large retail chain.

5. Ask About a 90-Day Supply

Many pharmacies and most Medicare Part D plans offer a lower per-unit cost when you fill a 90-day supply rather than a 30-day supply. Under the Medicare cap, a 90-day supply of a covered insulin is generally capped at $105 — or potentially less if your specific insulin is subject to a negotiated price that produces lower cost-sharing. Mail-order pharmacies often offer a 90-day supply at a reduced monthly cost. Ask your plan or pharmacist what works best for your situation.

6. Request Samples from Your Doctor

If you are starting insulin for the first time or switching to a new type, ask your doctor’s office whether samples are available. Pharmaceutical representatives regularly leave sample vials and pens with physicians’ offices. A few weeks of free samples can give you breathing room while you work out the most affordable long-term plan.

7. Look Into State Insulin Copay Caps

As of 2025, 29 states and the District of Columbia have passed laws limiting insulin copays for commercially insured patients, with caps ranging from $25 to $100 per month depending on the state. Research shows these state caps had more limited effects than the federal Medicare cap — likely because most commercially insured patients were already paying less than $35 per month for insulin before the caps took effect. If you live in a capped state and are being charged more than the legal limit, contact your insurance provider. Check the American Diabetes Association’s state insulin copay cap tracker for your state’s current limit.

8. Appeal Your Insurance Formulary Decisions

If your insurance plan does not cover your prescribed insulin or places it on a high-cost tier, you have the right to appeal. Your doctor can submit a prior authorization or exception request explaining why you need that specific insulin. This process may require persistence, but it can result in significantly lower costs — often moving your insulin from a high-cost tier to a preferred tier on your plan’s formulary.

9. Insulin Pumps and CGM Devices: A Note on Expenses

Insulin pumps and automated insulin delivery (AID) systems use a single rapid-acting insulin instead of separate long-acting and short-acting injections, which works well for some patients. Continuous glucose monitors (CGMs) can help you and your care team fine-tune your doses and catch patterns early. However, pump therapy and CGM devices are not reliably lower in cost — device and supply expenses can be substantial, and coverage varies widely by insurance plan. Talk to your diabetes care team about both the clinical fit and the likely out-of-pocket costs before making a decision.

What Should I Do If I Don’t Have Insurance?

If you have no insurance, your options are more limited but still available. Here are the most practical routes:

- Manufacturer list price reductions: Since 2023, all three major insulin manufacturers have voluntarily reduced their list prices by 70–80%. Because uninsured patients typically pay the list price at the pharmacy, these reductions directly lower costs.

- Patient assistance programs: Each manufacturer offers a program for low-income, uninsured patients. You can apply directly on their websites or ask your doctor’s office to help with the application.

- Community health centers: Federally Qualified Health Centers (FQHCs) provide care to patients regardless of their ability to pay and often help coordinate access to affordable medications through the 340B drug pricing program.

- State pharmaceutical assistance programs: Some states help low-income residents pay for medications even without Medicaid. Check with your state health department.

- Lower-cost human insulin at Walmart: ReliOn NPH and Regular insulin are available without a prescription for about $25 per vial — potentially a short-term emergency option, but only with your doctor’s guidance, since these insulins work differently from modern analogs.

Are There Any Risks When Switching to Lower-Cost Insulin?

Switching from one insulin product to another — even to a biosimilar or a lower-cost brand — always carries some risk of changes in how your body responds. Different insulins may have slightly different timing in how quickly they start working and how long they last. Blood sugar patterns that were stable on your previous regimen could shift.

If you do switch, your doctor will likely recommend:

- Checking your blood sugar more often, especially during the first few weeks.

- Adjusting your dose under medical supervision, not on your own.

- Using a continuous glucose monitor (CGM), if available, to catch unexpected highs or lows.

The slight rise in severe low blood sugar events observed in the 2026 JAMA study is a reminder that more consistent insulin use generally improves blood sugar control, but must always be paired with careful dose management. Know the signs: shakiness, sweating, confusion, or a reading below 70 mg/dL (3.9 mmol/L). Always keep fast-acting sugar — such as glucose tablets — nearby, and consult your healthcare provider before making any changes to your insulin regimen.

What About Costs for Other Diabetes Medications?

The $35 cap and related insulin cost measures apply only to insulin. Current ADA/EASD 2026 guidelines recommend that GLP-1 receptor agonists (such as semaglutide) and SGLT-2 inhibitors (such as empagliflozin) are often prioritized for many patients — especially those with significant concerns about weight, cardiovascular disease, heart failure, or kidney disease. However, insulin remains appropriate and important in many clinical situations, and these guidelines are not a one-size-fits-all recommendation.

GLP-1 medications remain expensive, but prices are changing quickly. List prices for brand-name GLP-1 drugs can still be very high without insurance, but direct-to-consumer, manufacturer, and federal access programs have created lower cash-pay options for some patients. As of June 2026, TrumpRx — a federal direct-to-consumer platform — lists discounted monthly prices for several GLP-1 medications, including Ozempic, Wegovy, and Zepbound, but eligibility, availability, and final pharmacy costs may vary. No FDA-approved generic GLP-1 medications are currently available in the United States.

Novo Nordisk has also announced a significant voluntary list price reduction for Wegovy, Ozempic, and Rybelsus — however, this reduction is scheduled to take effect January 1, 2027, not in 2026. If you are hoping to benefit from lower semaglutide list prices, confirm the effective date and any plan-level implications with your pharmacist or insurer.

Beginning July 1, 2026, CMS is launching the Medicare GLP-1 Bridge, which may give eligible Medicare beneficiaries access to selected GLP-1 medications for a $50 monthly copay. This program has eligibility requirements and operates outside the standard Part D payment flow, so the $50 copay does not count toward Part D out-of-pocket spending.

Patient assistance programs are also available for GLP-1 and SGLT-2 medications; ask your doctor or pharmacist about options. If you are struggling with both insulin and non-insulin medication costs, talk to your care team about which medications offer the most important benefits for your specific situation. The Medicare Part D annual out-of-pocket spending cap — $2,100 in 2026, applying to covered Part D drugs — may provide meaningful relief if your total drug burden is high.

What Should You Do Right Now?

If you are concerned about the cost of insulin, start with these steps:

- Talk to your doctor or diabetes care team about your expenses. They may be able to switch you to a lower-cost insulin or connect you with assistance programs.

- If you have Medicare, confirm that your plan covers your insulin and that your copay is $35 or less per month. If you use NovoLog or Fiasp, ask your plan whether the 2026 negotiated price brings your cost below $35. If you have questions, call 1-800-MEDICARE.

- If you are uninsured, apply for a manufacturer patient assistance program. Your doctor’s office can often assist with the paperwork.

- Use a price comparison tool like GoodRx to check if switching pharmacies could save you money immediately.

- Ask about biosimilar options — Semglee, Rezvoglar, Merilog, or Kirsty may be just as effective and more affordable. Ask your pharmacist whether an interchangeable biosimilar can be substituted under your state’s laws and your plan’s coverage.

- Never ration your insulin without consulting your doctor first. If cost is causing you to take less than prescribed, that is a medical issue that should be addressed promptly.

Helpful Resources and Research

- American Diabetes Association — State Insulin Copay Caps

- CMS Medicare Drug Price Negotiation Program — Negotiated Prices

- NeedyMeds — Patient Assistance Program Finder

- GoodRx — Pharmacy Price Comparison

- Mark Cuban Cost Plus Drugs

- TrumpRx — Federal Direct-to-Consumer Drug Platform: trumprx.hhs.gov (prices and eligibility subject to change; verify before use)

- Hong et al., JAMA Internal Medicine (April 2026): “Out-of-Pocket Spending for Insulin by Medicare Beneficiaries After Monthly Caps” — doi:10.1001/jamainternmed.2026.0255

- Hung, Inouye & Durant, JAMA Internal Medicine (April 2026): “Insulin Copay Caps — Impacts Beyond Costs” — doi:10.1001/jamainternmed.2026.0268

- ADA Standards of Care 2026: Section 9 — Pharmacologic Approaches to Glycemic Treatment

Frequently Asked Questions About Insulin Costs

How much should I be paying for insulin each month?

If you have Medicare, federal law limits your insulin copay to $35 per month for each covered insulin product under both Part B and Part D. A 3-month supply is generally capped at $105 — or potentially less if your insulin is subject to a 2026 negotiated price that produces lower cost-sharing. If you have private insurance, your costs vary by plan, but 29 states plus DC now cap insulin copays — usually between $25 and $100 per month. If you are uninsured, major manufacturers have significantly reduced list prices since 2023. A pharmacy price comparison tool like GoodRx can help you find the lowest cash price in your area.

Does the $35 Medicare cap cover all types of insulin?

The $35 cap applies to insulin on your Medicare Part D plan’s formulary (drug list) and insulin covered under Medicare Part B — typically insulin used in a pump. Most widely prescribed insulins, including long-acting types like glargine and degludec and rapid-acting types like aspart and lispro, are covered. Starting in 2026, some patients using NovoLog or Fiasp may pay less than $35 per month under the Medicare Drug Price Negotiation Program — check your plan’s formulary and pharmacy pricing for the exact amount. If your prescribed insulin is not covered, you can request a formulary exception.

Can I get insulin without a prescription and save money?

Walmart sells two older human insulins — ReliOn NPH and Regular — over the counter for about $25 per vial without a prescription. These are not the same as modern analog insulins and are not generic versions of them. They work on a different schedule, meaning your meal timing and dosing approach would need to change. Never switch insulin types without consulting your doctor first — doing so without guidance can lead to dangerous blood sugar swings in either direction.

Is biosimilar insulin safe and effective?

Yes. Biosimilar insulins are FDA-approved versions of brand-name insulins proven to be just as safe and effective. As of mid-2025, four insulin biosimilars are FDA-approved in the US: Semglee and Rezvoglar (for long-acting glargine/Lantus), and Merilog and Kirsty (both rapid-acting biosimilars to NovoLog, approved in 2025). Interchangeable biosimilars can generally be substituted at the pharmacy, subject to your state’s laws and your plan’s policies. Ask your doctor or pharmacist which option is right for your regimen and coverage.

What is an interchangeable biosimilar, and why does it matter?

An interchangeable biosimilar has met a higher FDA standard, demonstrating it can be substituted for the brand-name product at the pharmacy — similar to how a generic drug works — subject to state pharmacy laws and your insurance plan. For insulin, Semglee (long-acting) and Kirsty (rapid-acting, approved July 2025) carry interchangeable designation. Ask your pharmacist whether substitution is allowed for your prescription and state, as rules can vary.

Did the $35 Medicare cap lead more people to start using insulin for the first time?

Based on the 2026 JAMA research, the answer appears to be no — at least not yet. The study found that the share of type 2 diabetes patients beginning insulin did not increase during the study period. The main benefit was that people already on insulin used it more consistently. The companion editorial notes that copay caps alone may not be enough to overcome clinical inertia or patient hesitancy, and the growing role of GLP-1 and SGLT-2 medications as first-line options may also be a factor.

What should I do if my blood sugar drops too low after starting my full insulin dose?

A modest increase in severe low blood sugar (hypoglycemia) events was observed in the 2026 JAMA study as more patients began taking their full prescribed dose. Know the symptoms: shakiness, sweating, confusion, rapid heartbeat, or a blood sugar reading below 70 mg/dL (3.9 mmol/L). Always keep fast-acting sugar — such as glucose tablets or juice — nearby. If you are increasing your insulin dose or switching products, work with your doctor to adjust carefully, and consider using a continuous glucose monitor (CGM) to catch unexpected lows early.

Are state insulin copay caps as effective as the Medicare cap?

Research shows that state caps for privately insured patients have had more limited effects than the federal Medicare cap. The main reason: most commercially insured patients were already paying less than $35 per month for insulin before the caps took effect. The Medicare cap was more impactful because over 62% of Medicare insulin users were paying more than $35 for a 30-day supply before it was enacted.

Why did my spending on other diabetes drugs go up even though insulin got cheaper?

The 2026 JAMA research found that while insulin costs dropped for Medicare patients, spending on non-insulin diabetes medications — like GLP-1 drugs and SGLT-2 inhibitors — increased during the same period. The companion editorial emphasized that overall medication affordability can remain a challenge even when insulin costs improve. GLP-1 pricing is changing rapidly in 2026 through new federal programs and manufacturer announcements — ask your doctor or pharmacist about your current access options, including TrumpRx and manufacturer assistance programs.

I can’t afford my insulin right now. What should I do immediately?

If you are out of insulin or nearly out, call your prescriber the same day, contact the manufacturer’s emergency assistance program, and ask your pharmacy whether an emergency supply is allowed under your state’s law. Beyond that: contact the manufacturer directly — Eli Lilly, Novo Nordisk, and Sanofi all have emergency assistance programs and have voluntarily reduced list prices since 2023. If you have Medicare, call 1-800-MEDICARE. For other help, visit NeedyMeds.org or ask your doctor’s office to assist you. If you are experiencing severe high blood sugar symptoms — extreme thirst, frequent urination, nausea, or confusion — go to the emergency room. Hospitals are required to stabilize patients regardless of ability to pay.

What is a patient assistance program and how do I apply?

Patient assistance programs (PAPs) are offered by drug manufacturers to provide free or reduced-cost medications to people who cannot afford them, typically based on income and insurance status. Each major insulin maker — Eli Lilly, Novo Nordisk, and Sanofi — has its own program. You can apply directly on the manufacturer’s website, or ask your doctor’s office to help. NeedyMeds.org lists programs from many manufacturers in one place and is a good starting point.

Last Updated on June 2, 2026